All Categories

Featured

Table of Contents

Keep in mind, nonetheless, that this doesn't claim anything about adjusting for rising cost of living. On the bonus side, even if you presume your alternative would be to buy the stock exchange for those seven years, and that you would certainly obtain a 10 percent yearly return (which is far from certain, specifically in the coming years), this $8208 a year would be greater than 4 percent of the resulting small stock worth.

Instance of a single-premium deferred annuity (with a 25-year deferral), with four settlement choices. The month-to-month payment here is greatest for the "joint-life-only" alternative, at $1258 (164 percent greater than with the prompt annuity).

The method you purchase the annuity will certainly figure out the solution to that inquiry. If you purchase an annuity with pre-tax bucks, your costs reduces your taxable income for that year. According to , buying an annuity inside a Roth plan results in tax-free payments.

Deferred Annuities

The advisor's very first step was to establish a comprehensive economic strategy for you, and then discuss (a) how the proposed annuity fits into your total plan, (b) what options s/he considered, and (c) exactly how such alternatives would certainly or would certainly not have caused lower or higher compensation for the consultant, and (d) why the annuity is the exceptional selection for you. - Tax-deferred annuities

Certainly, an advisor might attempt pushing annuities also if they're not the most effective suitable for your situation and objectives. The factor might be as benign as it is the only item they sell, so they fall target to the proverbial, "If all you have in your tool kit is a hammer, rather soon everything starts appearing like a nail." While the expert in this circumstance might not be dishonest, it enhances the risk that an annuity is a bad option for you.

Why is an Secure Annuities important for long-term income?

Because annuities often pay the representative offering them much higher payments than what s/he would obtain for spending your cash in common funds - Annuity income, allow alone the absolutely no commissions s/he 'd receive if you invest in no-load common funds, there is a huge motivation for agents to push annuities, and the a lot more complicated the better ()

A dishonest advisor recommends rolling that quantity right into new "better" funds that just take place to bring a 4 percent sales lots. Concur to this, and the expert pockets $20,000 of your $500,000, and the funds aren't most likely to do much better (unless you selected a lot more poorly to start with). In the exact same example, the advisor could guide you to buy a complex annuity with that $500,000, one that pays him or her an 8 percent compensation.

The advisor tries to hurry your choice, asserting the deal will certainly quickly go away. It might certainly, but there will likely be equivalent offers later on. The advisor hasn't found out exactly how annuity payments will be tired. The advisor hasn't revealed his/her payment and/or the charges you'll be billed and/or hasn't revealed you the effect of those on your ultimate payments, and/or the compensation and/or charges are unacceptably high.

Existing rate of interest prices, and thus predicted repayments, are historically reduced. Even if an annuity is ideal for you, do your due diligence in comparing annuities marketed by brokers vs. no-load ones sold by the issuing business.

How much does an Fixed Vs Variable Annuities pay annually?

The stream of month-to-month settlements from Social Safety and security is similar to those of a deferred annuity. Actually, a 2017 comparative analysis made a comprehensive contrast. The complying with are a few of the most prominent points. Considering that annuities are volunteer, the people buying them normally self-select as having a longer-than-average life expectancy.

Social Security advantages are totally indexed to the CPI, while annuities either have no inflation protection or at a lot of offer an established percentage annual rise that may or might not make up for rising cost of living in full. This type of biker, just like anything else that raises the insurance company's threat, needs you to pay even more for the annuity, or approve lower payments.

What is the best way to compare Tax-deferred Annuities plans?

Please note: This write-up is planned for informative purposes just, and must not be considered economic recommendations. You need to consult a financial specialist prior to making any kind of significant economic choices.

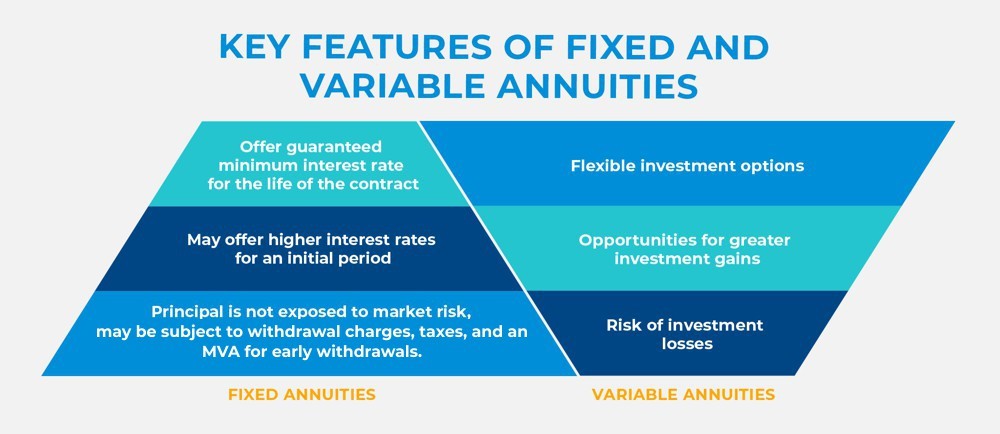

Since annuities are meant for retired life, tax obligations and fines might use. Principal Protection of Fixed Annuities. Never shed principal due to market efficiency as dealt with annuities are not spent in the market. Also throughout market recessions, your money will certainly not be influenced and you will not shed cash. Diverse Investment Options.

Immediate annuities. Deferred annuities: For those who desire to expand their cash over time, but are willing to defer accessibility to the cash until retirement years.

What should I look for in an Long-term Care Annuities plan?

Variable annuities: Supplies better possibility for development by investing your money in investment alternatives you choose and the ability to rebalance your profile based upon your choices and in such a way that aligns with transforming financial goals. With fixed annuities, the firm spends the funds and provides a rate of interest to the customer.

When a fatality case happens with an annuity, it is essential to have actually a called beneficiary in the contract. Different alternatives exist for annuity survivor benefit, depending upon the contract and insurance provider. Picking a reimbursement or "period specific" choice in your annuity supplies a survivor benefit if you pass away early.

What should I look for in an Fixed-term Annuities plan?

Naming a recipient various other than the estate can aid this process go extra smoothly, and can assist make sure that the profits go to whoever the private wanted the cash to go to instead than going with probate. When existing, a death advantage is instantly consisted of with your contract.

{kind=link}

Table of Contents

Latest Posts

Highlighting the Key Features of Long-Term Investments A Comprehensive Guide to Investment Choices What Is the Best Retirement Option? Features of Fixed Index Annuity Vs Variable Annuities Why Choosin

Analyzing Strategic Retirement Planning Everything You Need to Know About Financial Strategies What Is Indexed Annuity Vs Fixed Annuity? Pros and Cons of Choosing Between Fixed Annuity And Variable An

Analyzing Strategic Retirement Planning A Comprehensive Guide to Fixed Vs Variable Annuity Pros And Cons Defining the Right Financial Strategy Pros and Cons of Various Financial Options Why Choosing t

More

Latest Posts